I first came across Creative Newtech when using my version of the ‘Canslim’ screener in screener.in :

Market Capitalization > 50 AND

YOY Quarterly profit growth > 20 AND

Sales growth 5Years > 20 AND

Profit growth 5Years > 20 AND

Unpledged promoter holding > 50 AND

RSI > 50

Company : Creative Newtech Ltd

Mcap : 1260 cr

About the company

A writeup / summary of the company that I came across covers it pretty well:

My conclusion : A good company with the possibility of good headroom for growth while not paying too much for it.

The % of market cap which accounts for what is already there and what can reasonably be expected is at least ~75%

Premium for the ‘uncertain’ / future growth aspect, bet on ‘Gen -Z’, high margin products is ~25% – I feel the company is on the right track to achieve this and probability of it materialising is high.

It doesn’t seem overvalued for where it currently is at and looks undervalued for where it is headed.

Main thesis :

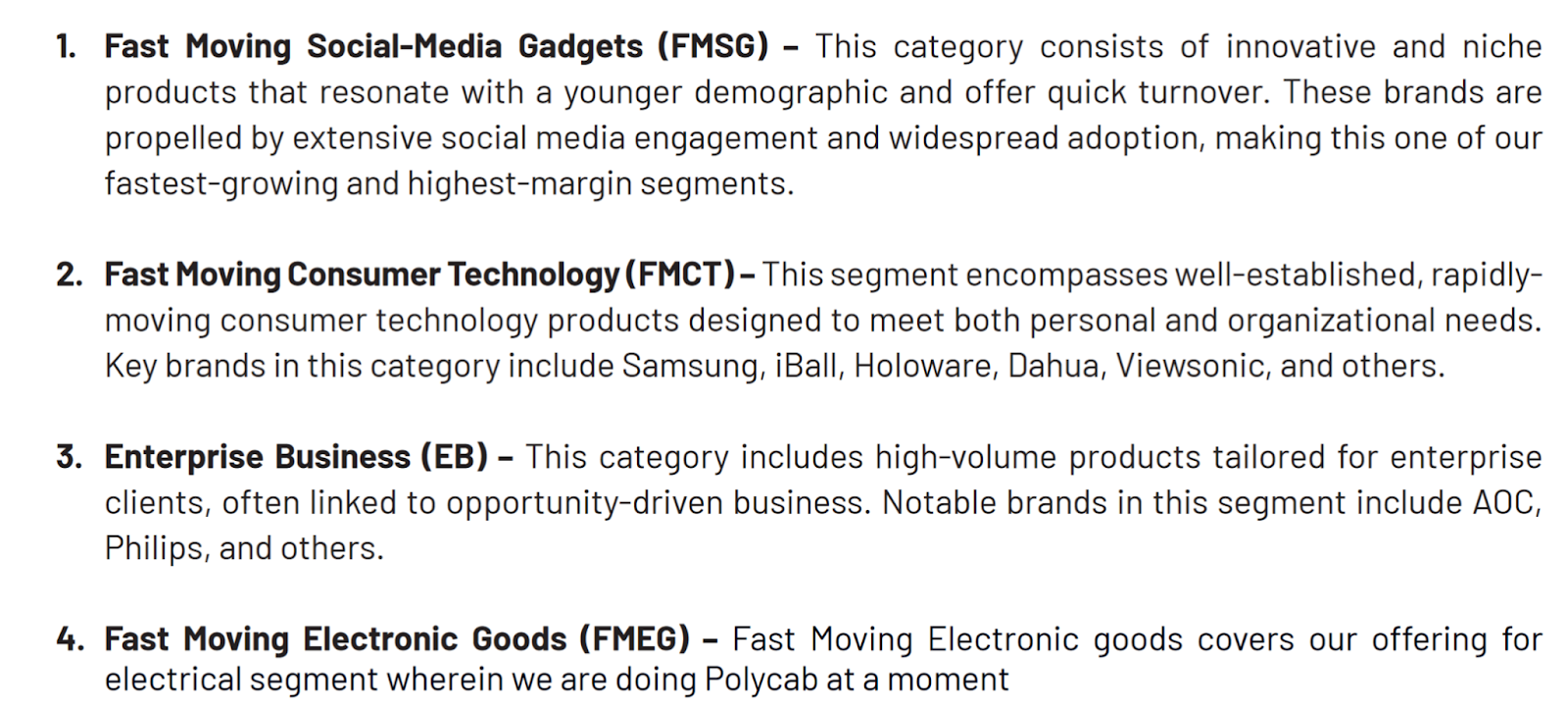

- Company operates under 4 categories :

From the latest AR :

- Enterprise Business, currently 70% of the total revenue

- With FMSG : 15%, FMCT : 15%, FMEG : None for now (looking to piggyback polycab to enter south indian markets)

- The EB business is low margin ~2-3%

- The FMSG part is high margin ~10-40% and ‘futuristic’ with a lot of potential

A video of the owner talking about this :

ELI – 356 | Ketan Patel (Founder of Creative Newtech Limited)

- FMEG margins : ~<10% but well established and proven products and brands

- Transition which will create value :

- shift from low margin, EB business to the other, higher margin segments

- Shift from B2B to a more direct to customer approach

I think there is no going back with things like Social Media and Computers… With the advancement of AI and other computer based technology, and with the newer generation (18-25 yr old such as myself) entering into an earning phase, I anticipate that the need for these “FMSG” products will grow. I think the company is situated in the right place to make use of this when it actually materialises in the near future (and you’re not paying too much for this)

Need for these new products grows → Newer brands want to enter Indian markets → Creative Newtech’s existing position helps it grow (both Topline and margins and thus the bottomline)

The kind of products that fall under the high margin FMSG side : A bet on GEN – Z

- Audio devices/ brands like Beats by Dre, speakers

- Go-Pros for Vloggers

- Gaming devices and gadgets to capitalise on growing Esports scene

Main risks :

- Relationship with the brands… The company relies a lot on brands like Honeywell – Issues with brands can disrupt the sales and profitability significantly.

- Lack of cash generation. Has always been negative but the company is growing at a good pace.

- Very low margin on sales (expected to improve)

Margins

- 3% OPM consistently : Mainly due to 70% revenue from Enterprise Business (which does around 2-3%)

- Tldr : Expected to improve as the company does more “FMSG” sales… cause for concern if it remains same in subsequent years

- Company considers : Cyberpower (gaming PCs) and Honeywell as FMSG.

- Revenue growth in FMSG cagr : 11%

- In 2020, secured an exclusive licence from Honeywell to manufacture and sell a variety of products, including cables, adapters, audio products, and air purifiers

- Growth of revenue from Honeywell :

FY22:61 cr to FY24:170 cr ; As % of revenue : 6.8% vs 10.32%

- Honeywell’s business is high margin ~ 34-38%. The Honeywell side is expanding.

- Mgmt :

- “Honeywell business should become a Rs. 500 crores business in the next 2 years to 3 years”

- Going forward in coming years as our aspiration is to grow Honeywell and we are working very hard towards that and if that happens, then within 2 years-3 years the PAT margins will look in the range of 4.5% to 5.56%. That is going to be our endurance.